When Systemic Risk Meets Polyexponential.ai Intelligence

_______________

Global Pioneer in AI-Driven Systemic Risk Intelligence and Gloabl Macro Quantamental Investing Solutions. Founded in 2019, with a panel of PhD experts from University of Georgia, Peking University, North Carolina State University, Oxford University, Imperil London College.

Polyexponential.ai decodes financial fragility through causal AI and adaptive macro multi-strategies, ensuring you stay ahead in a volatile market.

Vision: Build the immune system for global macro multi-strategy system. Transparent model governance, human-in-the-loop validation and governance.

Empower Your Financial Future

At Polyexponential.ai, we harness cutting-edge AI technology to transform systemic risks into actionable insights. Join us in building a resilient financial landscape where innovation meets integrity, ensuring your investments thrive in any market condition.

Transforming Risk into Strategic Advantage

At Polyexponential.ai, we leverage cutting-edge AI technology to decode financial fragility and enhance market resilience. Our expert team combines deep research with practical strategies, ensuring that our clients navigate systemic risks effectively while maximizing their investment potential. Join us in redefining the future of finance through intelligent solutions.

Insights & Research

_____________________________________

Innovative Solutions

Expert Insights

Data-Driven Strategies

Cutting-Edge Research

Systemic Risk Intelligence

Empowering Financial Resilience

Don’t predict the future. Evaluate the present fragility.

*This module details the historical backtested results and performance characteristics of the system, framed purely as a deployable, installable technology. We understand that your data is your most secure asset. Polyexponential.ai is engineered as a zero-leak, locally deployable technology infrastructure. Access real-time systematic case studies, macro structural updates, and network vulnerability profiles mapped by our installable engine.

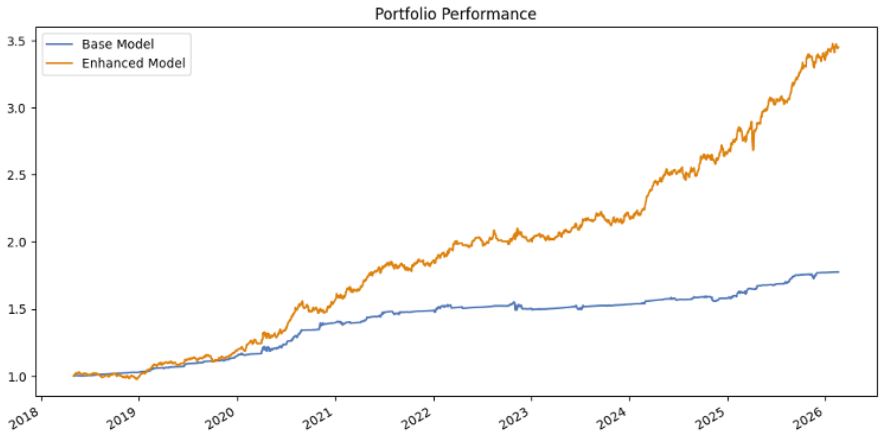

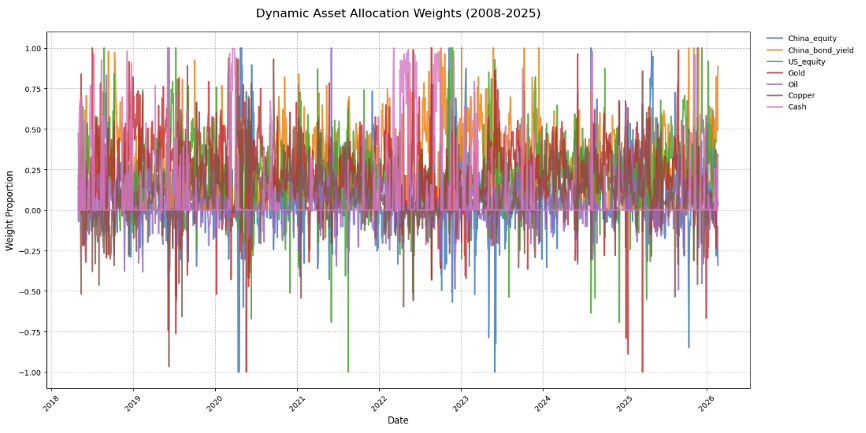

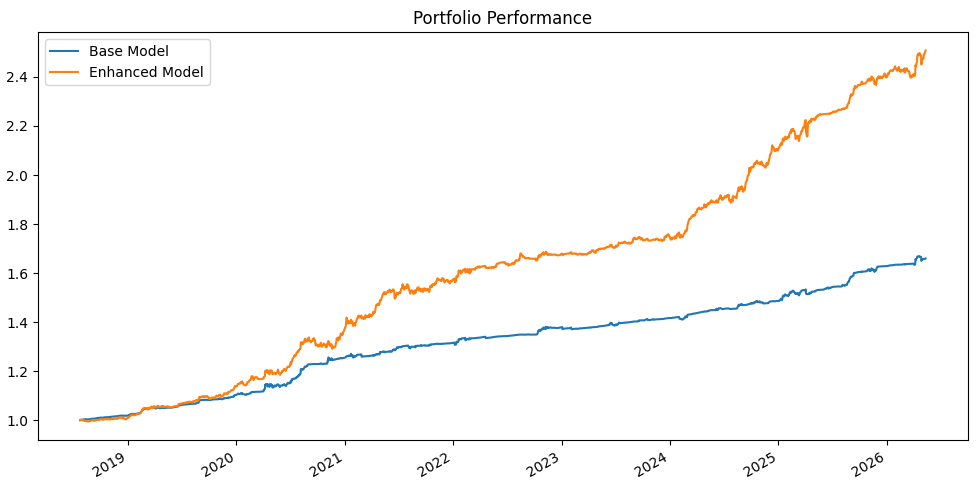

State of the Art Macro Risk Controlled Risk Parity Model for Macro Multi-Strategy Funds.

The backtest metrics of the long-only macro risk controlled model:

The Base Risk Budget Model(Blue) Annual Return: 7.38%

The Macro Risk Controlled Model(Orange) Annual Return: 16.61%

The Base Risk Budget Model Win Rate: 71.13%

The Macro Risk Controlled Model Win Rate: 57.68%

The Base Risk Budget Model NAV: 1.77

The Base Risk Budget Model Sharpe Ratio: 1.88

The Base Risk Budget Model MaxDrawdown: 4%

The Macro Risk Controlled Model NAV: 3.45

The Macro Risk Controlled Model Sharpe Ratio: 1.91

The Macro Risk Controlled Model MaxDrawdown: 7%

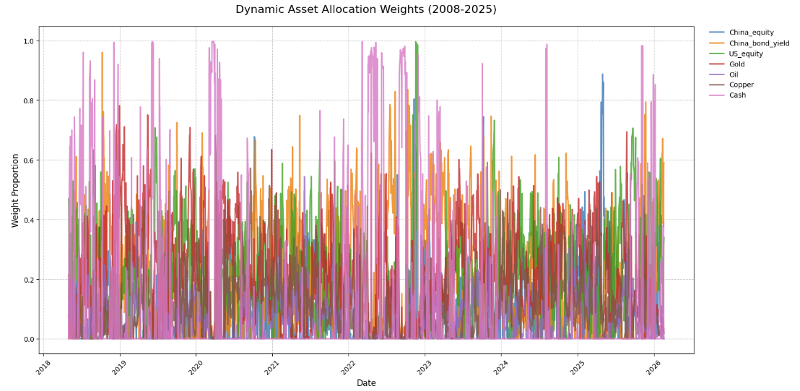

The long-only macro risk controlled model dynamic asset allocation weights

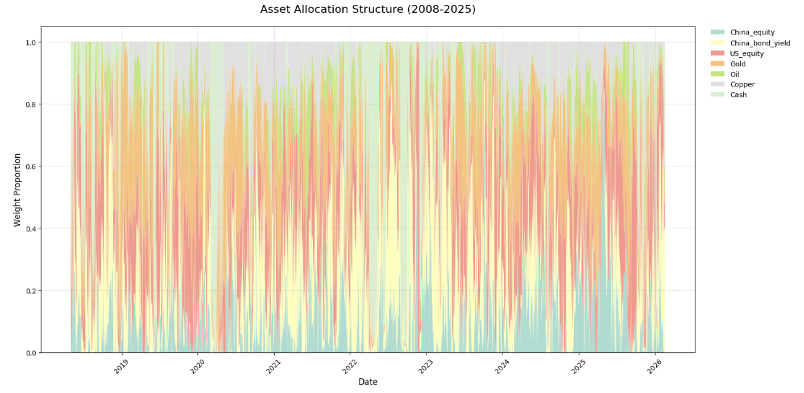

The long-only macro risk controlled model asset allocation structure

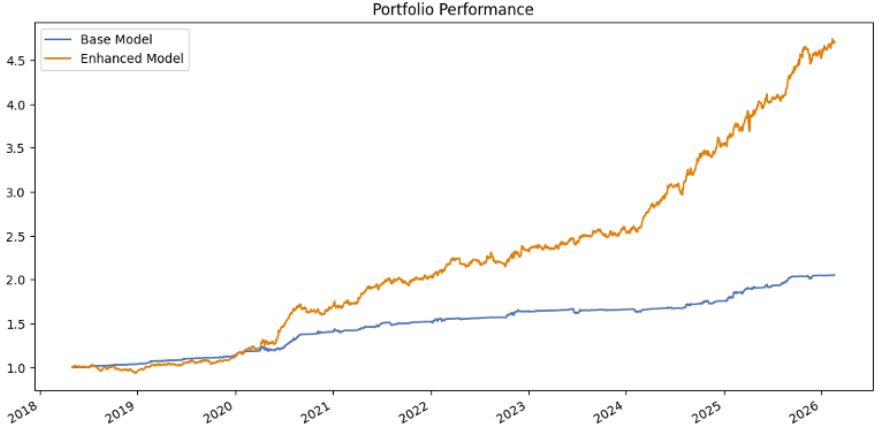

State of the Art Macro Risk Controlled Risk Parity Model for Macro Multi-Strategy Funds.

The backtest metrics of the long-short macro risk controlled model:

The Base Risk Budget Model(Blue) Annual Return: 9.33%

The Macro Risk Controlled Model(Orange) Annual Return: 21.21%

The Base Risk Budget Model Win Rate: 67.44%

The Macro Risk Controlled Model Win Rate: 56.11%

The Base Risk Budget Model NAV: 2.05

The Base Risk Budget Model Sharpe Ratio: 2.26

The Base Risk Budget Model MaxDrawdown: 4%

The Macro Risk Controlled Model NAV: 4.71

The Macro Risk Controlled Model Sharpe Ratio: 2.08

The Macro Risk Controlled Model MaxDrawdown: 9%

Long-short investment phase dynamic asset allocation weights

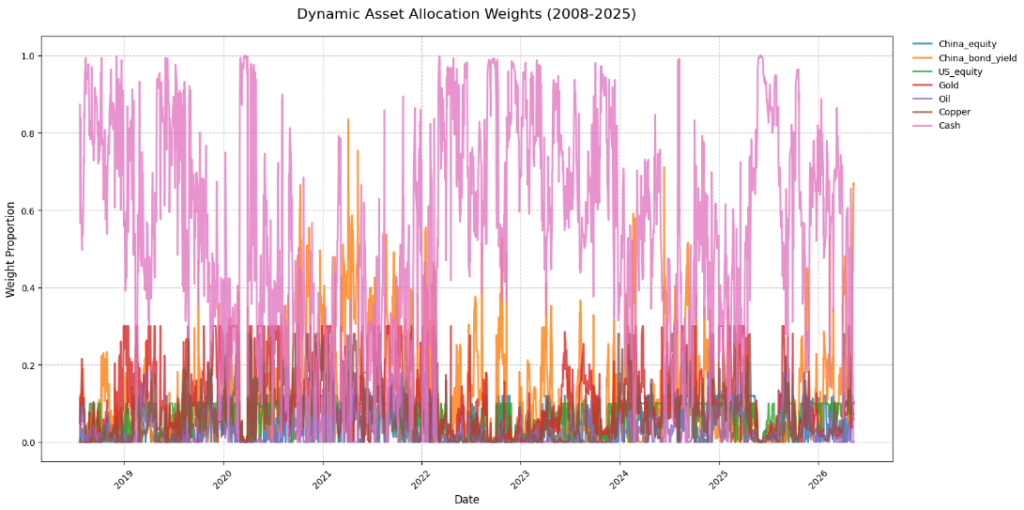

State of the Art Macro Risk Controlled Risk Parity Model for Macro Multi-Strategy Funds.

The optimal constraint investment phase backtest metrics of the long-only macro risk controlled model:

The Base Risk Budget Model(Blue) Annual Return: 6.48%

The Macro Risk Controlled Model(Orange) Annual Return: 12.08%

The Base Risk Budget Model Win Rate: 70.79%

The Macro Risk Controlled Model Win Rate: 60.64%

The Base Risk Budget Model NAV: 1.66

The Base Risk Budget Model Sharpe Ratio: 2.79

The Base Risk Budget Model MaxDrawdown: 1%

The Macro Risk Controlled Model NAV: 2.51

The Macro Risk Controlled Model Sharpe Ratio: 2.55

The Macro Risk Controlled Model MaxDrawdown: 3%

The optimal constraint investment phase dynamic asset allocation weights of the long-only macro risk controlled model

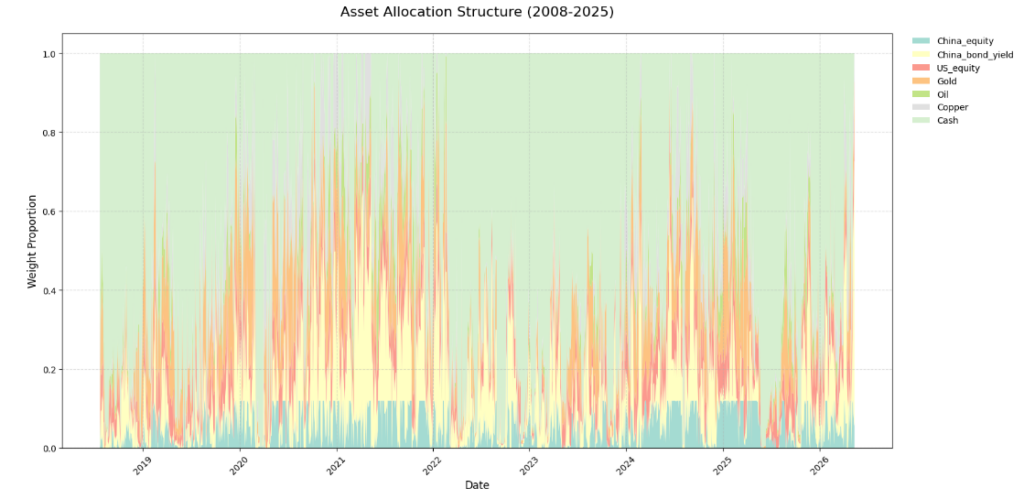

The optimal constraint investment phase asset allocation structure of the long-only macro risk controlled model

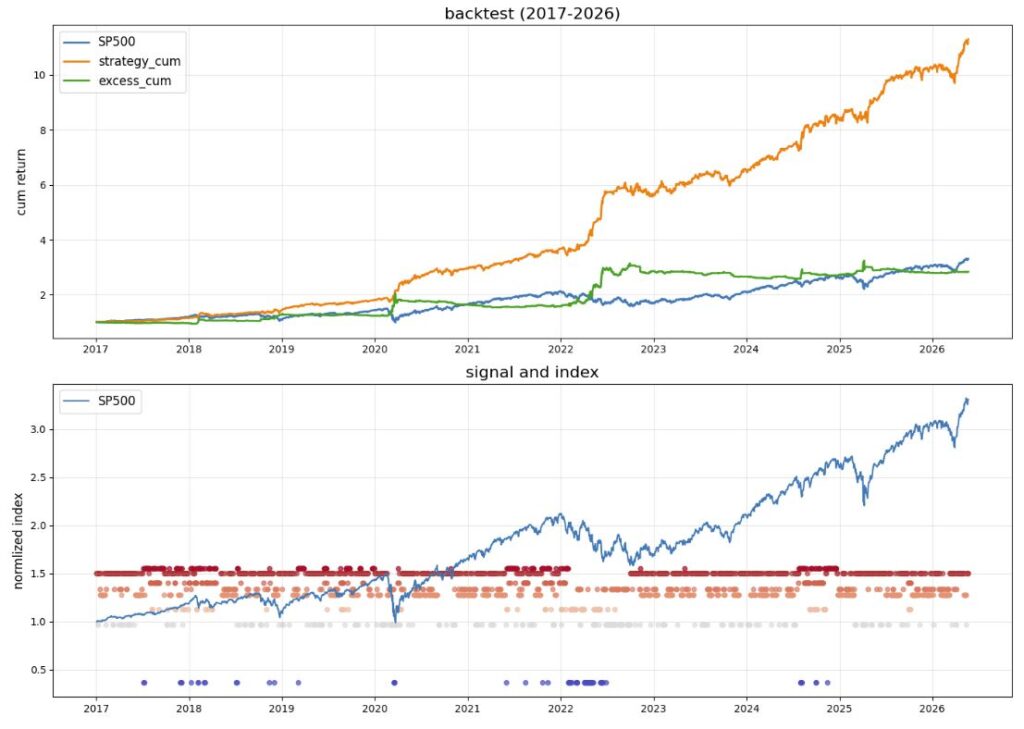

Systematic Integration of Systemic Risk Management and Multi-Factor Pricing Dynamics in S&P 500 Price Discovery.

The backtest metrics of SP500 model:

Strategy Total Return: 1030.43%

Strategy Annual Return: 29.51%

Strategy Excess Return: 183.40%

Strategy Annual Excess Return: 11.75%

Strategy Sharpe Ratio: 1.9

Strategy MaxDrawdown: 8.54%

Research insights:

- Systematic Integration of Systemic Risk Management and Multi-Factor Pricing Dynamics in S&P 500 Price Discovery. *Polyexponential.ai Copyrights reserved.

- State of the Art Macro Risk Controlled Risk Parity Model for Macro Multi-Strategy Funds. *Polyexponential.ai Copyrights reserved.

- A global asset allocation system based on a macro alternative multi-factor rating model. Patent Pending. *Polyexponential.ai All rights reserved.

- An all-weather global asset allocation system. Patent Pending. *Polyexponential.ai All rights reserved.

Professional Plan

$59,999

per month

Perfect for individuals who want to manage their finances.

Institutional Plan

$690,000

Starting quote

Designed for larger businesses and organizations.

Technology Infrastructure & Advisory Disclaimer: Polyexponential.ai is an advanced financial technology developer, structural system designer, and mathematical intellectual property licensor. We are not a registered investment advisor, asset management fund, or licensed broker-dealer. We do not accept client capital for management, execute financial market trades, or provide personalized investment or financial planning advice. All installable systems, desktop packages, local visualization engines, and consulting frameworks are designed exclusively for quantitative research, infrastructure upgrades, and institutional risk evaluation. Performance data displayed reflects mathematical simulations and extensive historical backtesting in controlled environments.

Intellectual Property & Security Compliance: Our global asset allocation and risk evaluation systems are legally protected under several patents. System installation protocols are fully compliant with SOC 2 Type II data safety frameworks, GDPR, and CCPA standards. Local installations require valid cryptographic hardware verification keys to prevent unauthorized IP distribution.

Partnership opportunities: Patent Licensing, Joint Lab Creation

“Risk never sleeps. Neither does our intelligence.”

— Polyexponential.ai: Where exponential minds safeguard exponential value.